With the rapid development of China’s economy in recent years, China’s polyester industry has gradually improved its global market position. Data shows that China’s polyester production has increased its global share from 43.54% to around 64.35% in more than ten years.

Global and Chinese polyester production from 2010 to 2020:

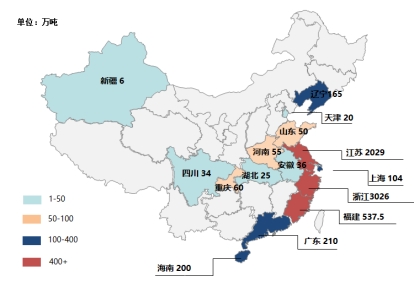

China is the global polyester production and consumption center, and Jiangsu and Zhejiang are China’s main polyester production areas. As can be seen from the figure below, the polyester production capacity of Zhejiang and Jiangsu provinces accounts for approximately 77% of the country’s total polyester production capacity.

China’s polyester production capacity distribution map in 2021:

Zhejiang is the largest production and sales province, and Zhejiang is mainly concentrated in Huzhou, Xiaoshao, and Ningbo areas, and the layout of the polyester industry is relatively concentrated.

Production capacity of the top 10 polyester manufacturers in China (unit: 10,000 tons):

The current CR10 industry concentration in the polyester industry has increased from 54.2% in 2019 to the current 61.9%. According to Longzhong statistics, it is expected that CR10 will further increase to 80% in 2023 above. According to the classification standards of industrial concentration by American economist Bain and the Japanese Ministry of International Trade and Industry, the industrial market structure is roughly divided into two types: oligopoly (CR10 ≥ 40%) and competitive type (CR10 < 40%). Among them, the oligopolistic type is further subdivided into extremely high oligopolistic type (CR10 ≥ 70%) and low concentration oligopolistic type (40% ≤ CR10<70%); the competitive type is further subdivided into low concentrated competitive type (20% ≤ CR10<40 %) and dispersed competitive type (CR10<20%). Applying this theory, the current industrial concentration of China's polyester industry can be classified as low concentration and oligopoly.

In the current international economic situation, high industry concentration means that the comprehensive competitiveness of the industrial chain has been enhanced, and competition among enterprises has become increasingly fierce. As far as polyester filament is concerned, the industry is highly concentrated, and larger companies play a leading role in the market, jointly promoting market development and maintaining industry profit levels, which to a certain extent is also beneficial to the healthy and stable development of the industry. In the future, the competition in the polyester market will further intensify, the granularity of enterprise operations will be refined, and cost control will become more stringent. Polyester production enterprises will lengthen and broaden the industrial chain through horizontal or vertical integration, with large scale, strong strength, and supporting industrial chain. Well-established companies will have more say. Therefore, in the future polyester industry, brand effect and large-scale development will be important bargaining chips for companies to compete for the market. </p