Crude oil prices maintained a narrow range of oscillation last week, showing that the current market logic is unclear. After the hurricane, changes in the crude oil market were relatively cautious. With U.S. supply and demand uncertain, the market chose to wait and see. However, as the weekend approached, the crude oil market suddenly became turbulent. The bulls who relied on inventory as their logic met the bears who relied on China’s release of reserve inventories as their logic. The market moved forward in the game.

Crude oil bulls saw a sharp decline in API inventory data, and expected EIA data to be equally bullish. After all, the US hurricane not only affected US refinery demand, but also affected US supply, so in Before the EIA data, crude oil bulls began to push up all the way, seeming to want to use the east wind of the EIA to push oil prices back to around US$75/barrel.

Before the EIA data, China suddenly announced that it would release national reserve inventories to cope with excessive oil prices and solve the crude oil shortage problem of some companies. The market fell sharply after hearing the news. Although the EIA data performed very well, bulls no longer dared to support the price again.

In addition to these factors, there was also news in the market last week that the United States had secretly had in-depth contacts with Iran and Venezuela, and had already revealed its intention to deal with Iran and Venezuela before Biden came to power. Lifting sanctions does not rule out the possibility that bad news about Iran and Venezuela will suddenly appear at some point. This is something we need to pay close attention to.

Taken together, crude oil prices have risen again after the news of China releasing crude oil reserves. Although oil prices have maintained a defensive oscillation trend in the short term due to the slow resumption of production in the Gulf of Mexico, the outlook for the crude oil market is that There is a greater risk. With the expected growth rate of the demand side declining and the supply side slowly recovering, the crude oil market is still facing greater pressure. In September, according to seasonality, crude oil has reached the high point of the year, and the demand for crude oil will gradually decline in the future. From a fundamental point of view, the future period is not optimistic. From a macro perspective, the current bullish atmosphere is no longer as strong as before, and under expectations of currency tightening, crude oil prices will most likely continue to be under pressure. Therefore, under the current relatively high level, we must beware of potential downside risks in crude oil prices.

China is about to release crude oil reserves Inventory to curb excessive rise in oil prices

The biggest news in the market last week was that China was about to release its crude oil reserve inventory. With the approval of the State Council, the State Administration of Grain and Material Reserves organized the release of national reserve crude oil in phases and batches in a rotational manner for the first time. This release is mainly aimed at domestic refining and chemical integration enterprises to alleviate the pressure of rising raw material prices on production-oriented enterprises. Implementing regular rotation of national oil reserves is an important way to play the regulatory role of the reserve market. Putting national reserve crude oil on the market through open bidding sales will better stabilize the supply and demand in the domestic market and effectively protect national energy security.

After the news was released, bulls instantly felt the seriousness of the situation. Oil prices plunged sharply during the session. Even the bullish EIA data could not save oil prices.

China’s main target for releasing reserve stocks is refining and chemical integration projects. Before this news was released, Shenghong issued a company announcement stating that it has obtained the qualification for the right to use crude oil. “In order to ensure the smooth production and operation of the project, it is agreed in principle that Shenghong will use 16 million tons of imported crude oil per year, including 2 million tons of imported crude oil in 2021, 15.89 million tons of imported crude oil in 2022, and 16 million tons of imported crude oil starting in 2023. “This may mean that the fourth batch of crude oil import quotas that the market has been anticipating will most likely come to nothing. If this is the case, then the bulls’ fantasy of a rapid recovery in China’s crude oil imports in the fourth quarter will come to nothing. After all, in the previous market, the market also hyped this news, and the bulls also successfully pushed up crude oil prices through this news. .

Due to the impact of the epidemic last year, international oil prices plummeted. China took the opportunity to purchase a large amount of crude oil inventories. In addition to part of these crude oil inventories entering commercial reserves, a large part entered national reserves. Inventory, this time the country releases inventory, which means that the level of national reserve inventory is much higher than in previous years, and the country also has a certain confidence to release inventory to stabilize the risk of rising prices. As of the end of August, China’s onshore inventory levels stood at 960 million barrels, compared with 870 million barrels in the same period in 2019, according to data from Kayrros.

Kpler analyst Janus Juay in Singapore said that on September 8, China’s offshore crude oil storage was 59 million barrels, while on August 29 it was 41 million barrels. The increase Included are Middle Eastern grades such as Iraq’s Basra Light, Saudi Arabia’s Arabian Ultra Light, Abu Dhabi’s Das and Oman, as well as Venezuela’s Meri and Colombia’s Castilla. Overall, Singapore, Malaysia and China have 83.5 million barrels of oil stored offshore, which means that in addition to domestic onshore stocks, China also has a large amount of floating storage to use.

Both the United States and India have previously announced the release of reserve inventories, but the impact on oil prices is obviously not as big as China’s this time, and the market still focuses on China. According to Goldman Sachs’ forecast, the world’s�The balance between crude oil supply and demand will remain tight. China’s tightening of quotas and the release of inventories will inhibit demand growth to a certain extent, and the corresponding demand growth expectations will also be lowered. This may be more conducive to the global market returning to a balance between supply and demand. within the pattern. If this is the case, the $80/barrel target predicted by Goldman Sachs may become a more difficult goal to achieve. After all, as the supply side gradually recovers, if the growth rate of the demand side slows down and China’s imports decline, then the market will not With so much crude needed, the market will rebalance even more quickly.

This time the country releases reserve stocks for rotation, which means that at some point in the future, the country will still purchase a large amount of crude oil to increase inventory levels. As for when to make purchases, it depends on when crude oil prices can reach a relatively low point. Last year, the country made large purchases at low points, mainly from May to September. At that time, the average price of crude oil was 35-45 US dollars per barrel. Now the price has risen to above 70 US dollars per barrel. From the perspective of national strategic reserves, it is appropriate to sell reserves when oil prices are high to stabilize prices, and then replenish reserves when crude oil prices are low. This operation can not only stabilize commodity prices, but also maximize the value of inventory.

So in the future we must focus on changes in China’s crude oil imports. According to common sense, the reduction of import quotas will slow down the increase in China’s crude oil imports. If a certain period in the fourth quarter At this time, China’s import volume suddenly increased sharply, which may mean that China began to replenish its national reserves. There is a high probability that it will be the bottom range of the crude oil market at that time.

There is uncertainty in U.S. crude oil data

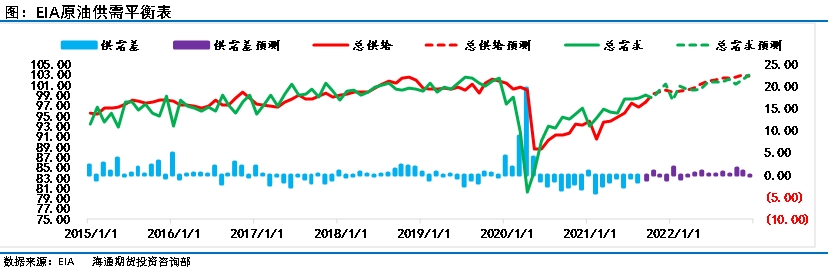

Last week’s U.S. crude oil inventory data also deserves our attention. Before the data was released, the market had expected that inventories might fall sharply last week. After all, there is no doubt that refined oil inventories will decline amid disruptions in refinery demand. At the same time, the recovery of drilling platforms in the U.S. Gulf has been extremely slow, and the impact on the supply side has not yet fully recovered. The decline in the supply side will also lead to a decline in crude oil inventories.

EIA inventory data shows that crude oil inventories fell by more than 1.5 million barrels, gasoline inventories fell by more than 7 million barrels, refined oil inventories fell by more than 3 million barrels, and full-bore inventories fell by 11 million barrels. Above, this is a relatively large decline. The decline in refined oil inventories has created the largest weekly decline in the past six months.

U.S. crude oil production fell by 1.5 million barrels in this period, returning to 10 million barrels. This is the largest weekly decline in U.S. crude oil production in history, which means that The impact of this hurricane is greater than any previous year. According to market reports, U.S. drilling rigs are still slowly recovering and are expected to recover more slowly than in previous years. Financial blog Zero Hedge said that only 20% of offshore platforms have been evacuated, but 77% of oil production is still shut down. One of the reasons for the slow recovery in oil and gas supply is Louisiana’s Port of Fourchon, a key hub for oil and gas platforms that handles more than 18% of the state’s oil supply. As of September 7, work to resume port operations is still ongoing. middle.

This means that next week’s U.S. crude oil inventory and production data will still be affected by the aftermath of the hurricane. Now the market is focusing on whether U.S. refinery demand or U.S. drilling platforms are more important. A quick recovery will directly determine the trend of crude oil inventories in the coming period. In the current situation where macro logic is not obvious, fundamental logic will dominate oil prices. Therefore, changes in inventory levels will also have a huge impact on future market conditions.

Crude oil prices have been oscillating at the current position for more than two weeks, and market volatility is not obvious. In the macro market, the U.S. dollar index has been strengthening recently, and U.S. stocks have also been in a weak state. The macro market is not conducive for bulls to continue to attack the city. In terms of fundamentals, the recovery of OPEC supply is undisputed, and China’s crude oil imports are expected to decline in the future. Increased supply and declining demand are obviously unfriendly to fundamentals. Fundamentals now all depend on the U.S. market in the short term, so we have to pay close attention to news about the resumption of U.S. refineries and drilling platforms in the Gulf of Mexico.

Taken together, crude oil prices have risen again after China released crude oil reserves. Although oil prices have maintained a defensive oscillation trend in the short term due to the slow resumption of production in the Gulf of Mexico, the market outlook Face greater risks. With the demand side expected to see a decline in growth and the supply side slowly recovering, the crude oil market is still facing greater pressure. Seasonally speaking, crude oil in September has entered the high point of the year. There is a high probability that crude oil demand will gradually decline in the future. The fundamentals of crude oil are not optimistic for some time to come. From a macro perspective, the current bullish atmosphere is no longer as strong as before, and under expectations of currency tightening, crude oil prices will most likely continue to be under pressure.

/o:p>

On the whole, crude oil prices have risen again after China released crude oil reserves, although oil prices have remained stable in the short term due to the slow resumption of production in the Gulf of Mexico. The oscillatory trend is resistant to decline, but the market outlook faces greater risks. With the demand side expected to see a decline in growth and the supply side slowly recovering, the crude oil market is still facing greater pressure. Seasonally speaking, crude oil in September has entered the high point of the year. There is a high probability that crude oil demand will gradually decline in the future. The fundamentals of crude oil are not optimistic for some time to come. From a macro perspective, the current bullish atmosphere is no longer as strong as before, and under expectations of currency tightening, crude oil prices will most likely continue to be under pressure. </p