After May Day, commodity prices continued to soar under the leadership of black products, and new idioms for commodities that were updated every year such as “unarmed”, “turning stones into gold”, and “walking in the snow in search of coal” were successively spun online. , and PTA, which has always been known as the “small thread” of the chemical industry, has performed relatively weakly after the holiday, and the current basis is significantly weaker than before the holiday. The main reason is what the author has explained before – PTA currently has no demand. With obvious signs of improvement, there is no ability to generate a trending market. The low processing fees in the early stage have been restored to a certain extent by the manufacturers’ continuous production reduction behavior for one and a half months. However, the current spot processing fees of more than 500 yuan/ton have no further benefits. Support and the equipment has begun to resume production one after another – Oh, by the way, the price of acetic acid has also dropped by about 600 yuan/ton after the holiday. It is really difficult to continue to expand upward.

Figure 1 Year-on-year comparison of PTA spot processing fees from 2016 to 2021 (unit: yuan/ton)

From the balance sheet Look, no matter whether Yisheng New Materials can be put into production smoothly by the end of this month, it is a fait accompli that PTA’s destocking efforts this month are much less than last month. And if there is no new maintenance plan in June, PTA will be on the tired track again after June. library channel.

Figure 2 Monthly PTA supply and demand situation from 2018 to June 2021 (unit: 10,000 tons)

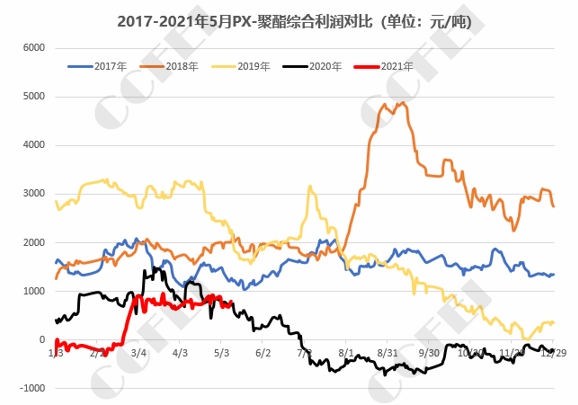

The current comprehensive profit of the industry chain Compared with the “tragic situation” after April last year, it has been repaired and has basically returned to the level before the epidemic last year. However, the overall profit situation still reflects the contradiction between the expansion of the industrial chain and the damage to the demand for alternative consumer goods. Recently, it is nothing more than internal profits. Since April, the processing fees of PX and PTA have been restored to a certain extent. Relatively speaking, the narrowing of the weighted profit of polyester is still relatively obvious, mainly concentrated in polyester chips, polyester staple fiber, and polyester bottle chips. In the early stage, due to the high degree of standardization, the secondary market stockpiling volume was relatively large, and it was focused on front-end products.

Figure 3 Comparison of PX-polyester comprehensive profit from 2017 to May 2021 (unit: yuan/ton)

Among them The cash flow of polyester chips has been at a loss for a month. Before May Day, some side slicing devices started to reduce production in advance. The production reduction has also intensified in the past two days. Yesterday, a major factory in Xiaoshan announced a daily production reduction of 500 tons. Shaoxing The first factory in Zhangjiagang has reduced production by 300 tons per day, and the first factory in Zhangjiagang has reduced production by 200 tons per day. Today, the five major polyester factories in Jiangsu and Zhejiang announced a joint production reduction of 3,000 tons/day of polymers (including FDY 2,000 tons/day, which has seen a sharp decline in profits recently). Another situation worth noting is the recent sharp rise in coal prices. The price of pit coal is now close to 1,000 yuan/ton, and it is already mid-May. If coal prices remain high, it may lead to large-scale power rationing this summer. In the current situation, the weaving end has been the first to bear the brunt of power cuts in previous years. We need to be alert to whether there will be sustained downstream production cuts from July to August.

With the rise in coal prices, the recent transaction focus of the chemical industry has undoubtedly shifted to more “coal” and less “oil”. Products such as ethylene glycol, methanol, and PP, which account for a large proportion of coal chemical industry, have been As a long position in the chemical industry, and seeing that May 21 is approaching the final time window of the Iran nuclear agreement, and the epidemic situation in India and other places has not seen substantial improvement, crude oil prices will still be dragged down by fundamentals, and there is a high probability that it will be temporarily It cannot outperform the black series and colored series that have better fundamentals, so it is highly correlated with crude oil, and its own fundamentals have made most of the profits. PTA undoubtedly assumed the market role of MEG last month – becoming A short-term standard empty allocation, but leaving aside the allocation perspective, it is still the same sentence. At the moment when demand cannot provide support, if PTA wants to move to a higher level, unless the supply side can provide more for the window period after June. “expect”. </p