This week, domestic and foreign cotton prices first rose and then fell, with the average price continuing to be higher than last week’s level; domestic cotton yarn prices continued to fall, while foreign yarn prices stopped rising and weakened; polyester staple fiber prices rose.

1. Domestic cotton prices first rose and then fell, with the average price higher than last week’s level

This week, affected by the new year’s seed cotton Boosted by expectations, domestic cotton prices fluctuated and rose. As the Zhengzhou Commodity Exchange adjusted the margin standards and price limits for some cotton futures contracts on Wednesday, domestic cotton prices stopped rising and weakened. From September 6 to September 10, 2021, the average settlement price of the main contract of cotton futures on the Zhengzhou Commodity Exchange was 17,878 yuan/ton, an increase of 427 yuan/ton or 2.4% from the previous week; the national cotton price represents the market price of standard grade lint cotton in the mainland. The average price of the B index was 18,123 yuan/ton, an increase of 194 yuan/ton from the previous week, an increase of 1.1%.

2. The increase in international cotton prices converged late in the week

This week, the market is worried about weather disturbances in the U.S. Gulf of Mexico and the possibility of late crops. The destruction stimulated the international cotton price to oscillate and rise, but then the market became cautious before the release of the USDA report, and ICE cotton prices weakened in late trading. From September 6 to September 10, 2021, the average settlement price of the main contract of the US Intercontinental Exchange Cotton Futures (ICE) was 93.78 cents/pound, an increase of 0.5% from the previous week, of the main contract settlement price of New York cotton futures. ; The average price of the International Cotton Index (M), which represents the average CIF price of imported cotton in China’s main ports, is 106.57 cents/pound, an increase of 0.92 cents/pound or 0.9% from the previous week, and the import cost in RMB is 17,190 yuan/ton (according to Calculated at 1% tariff (including Hong Kong miscellaneous goods and freight), it increased by 153 yuan/ton, or 0.9%, from the previous week. The international cotton price was 933 yuan/ton lower than the domestic cotton price, and the internal and external price difference expanded by 42 yuan/ton compared with last week.

3. The transaction price of reserve cotton increased

This week, the rotation of reserve cotton advanced steadily, and the transaction price increased slightly. From September 6 to 10, 2021, the average transaction price of reserve cotton was 17,207 yuan/ton, an increase of 212 yuan/ton from last week; the discounted standard grade (3128) price was 18,529 yuan/ton, an increase of 173 yuan/ton from last week. , an increase of 0.94%; among which, the average transaction price in Xinjiang was 17,303 yuan/ton, an increase of 257 yuan/ton, or 1.51% from last week, and the average transaction price of real estate cotton was 17,048 yuan/ton, an increase of 168 yuan/ton, or 1% from last week. .

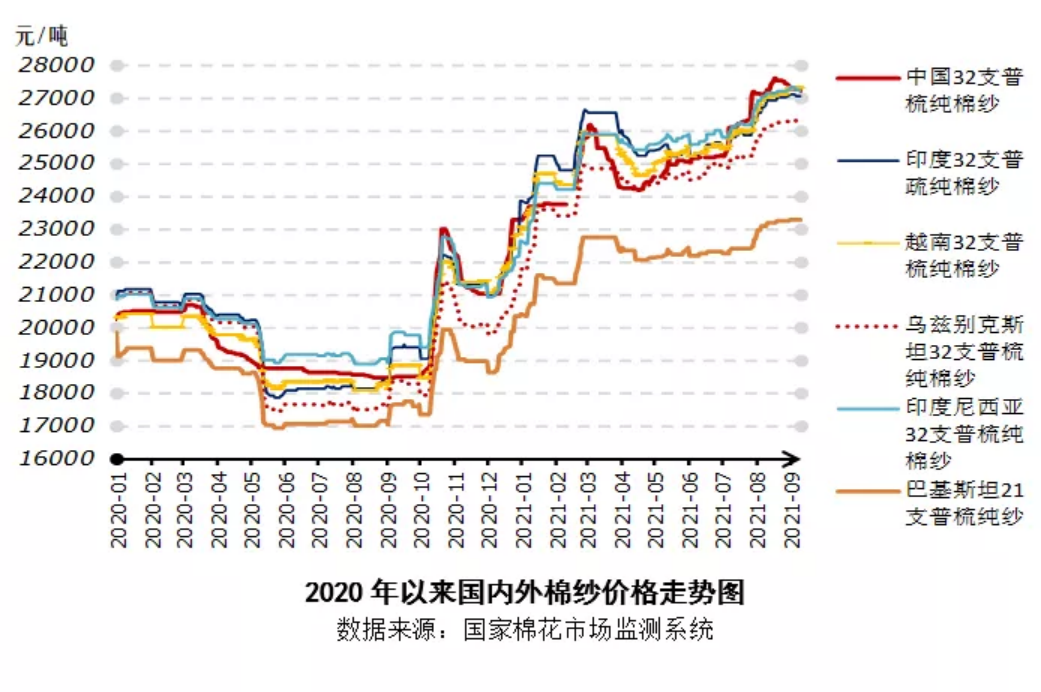

4. Cotton yarn prices at home and abroad have weakened

This week, orders in the textile market were lower than expected, and the traditional peak season of “Golden Nine and Silver Ten” did not appear, finished product inventories increased, and domestic cotton yarn prices continued to fall slightly. The international cotton yarn trading atmosphere subsequently weakened, and the price of imported yarn at Chinese ports was stable and weak. At present, the price of conventional foreign yarn is 53 yuan/ton lower than that of domestic yarn. Recently, orders for gray fabrics and printing and dyeing have generally been declining. Customers purchase on demand and dare not stock up in batches. The price of pure cotton cloth has remained stable.

5. Market outlook

Well-known international financial institutions have warned that U.S. stocks are facing There is a risk of correction, the northern hemisphere cotton harvest has begun, and the international cotton price trend is cautious. The European Central Bank will slow down the pace of its emergency bond purchase program in the fourth quarter. U.S. Treasury Secretary Yellen warned that if the debt ceiling fails to be raised in time, it may trigger financial system risks. Well-known international financial institutions such as Goldman Sachs and Morgan Stanley Warning that the current bull market in U.S. stocks faces the risk of a correction. In the international cotton market, the growth of US cotton has accelerated, and the boll-setting progress has reached 94%. The weather in southern Texas is ideal in the next week, and the harvest is advancing rapidly. The weather in the Gulf of Mexico is still uncertain; new cotton from northern India has also begun to be launched in small quantities; in the southern hemisphere Brazilian cotton harvest is 80% complete; according to the September global production demand forecast released by the International Cotton Advisory Committee (ICAC), global cotton production in 2021/22 is 24.93 million tons, a year-on-year increase of 3%, and cotton consumption is 25.87 million tons, an increase of 0.82%. Consumer demand for apparel is expected to fall further as the Biden administration’s federal unemployment benefits expire in September. Currently, global ports continue to be congested, causing supply chain chaos and reduced efficiency. It is expected that short-term international cotton prices will continue to fluctuate cautiously.

The acquisition of Xinjiang seed cotton is imminent, but the traditional downstream peak season has not appeared. The market mentality has become cautious, and domestic cotton prices have maintained a volatile trend. According to data from the National Bureau of Statistics, in August, the national consumer price index (CPI) rose by 0.8% year-on-year, and the industrial producer price index (PPI) rose by 9.5% year-on-year, hitting a new high since September 2008; the two increases were “scissors” apart. “Expanded, hitting a new high since data records began. This shows that raw material prices are running at a high level and there is no substantial transmission to the prices of end consumer goods. In terms of the domestic cotton market, cotton in Xinjiang continues to grow. According to data from the National Cotton Market Monitoring System, as of September 10, the national new cotton picking progress was 0.3%, a year-on-year decrease of 0.3 percentage points. Some ginning operations in Kashgar, Aksu and other places in southern Xinjiang Factory opening and scale acquisition, large-scale sales, processing, and sales have not yet officially begun. As the futures price of Zheng cotton increased, the outflow of warehouse receipts accelerated. As of September 10, the number of registered warehouse receipts for Zheng cotton was approximately 28.1 tons, a decrease of 28,800 tons from last week. As new cotton comes on the market, textile mills will be less willing to restock old cotton. The downstream peak season is obviously characterized by sluggishness. Cotton yarn traders in some areas have sold goods. Foreign trade orders have significantly weakened under the influence of the epidemic and tight shipping containers. Logistics experts believe that the phenomenon of early start of holiday orders such as Christmas has ended. In order to avoid risks, the market has a strong wait-and-see sentiment. Before the large-scale launch of new cotton,�Domestic cotton prices mainly fluctuated between stable and weak.

</p