[Introduction]: The recent performance of the polyester staple fiber market has continued to be flat, and low prices have been reported frequently in the market. However, the low point during the period did not induce a large-scale replenishment in the middle and lower reaches, but instead disrupted the replenishment rhythm of the downstream. At present, Spin mills are very cautious and conservative in their replenishment attitude, and frequent dip-hunting failures have also cast a shadow on the market, making the market seem to be trapped in a vicious cycle.

As of Friday, the polyester staple fiber spot price index fell to 6,855 yuan/ton, the lowest level in the past three months. However, with many failed attempts at bargain hunting, frequent price drops did not trigger concentrated stocking downstream. Moreover, the “Golden Nine” failed to go as scheduled, and downstream orders did not increase significantly. On the contrary, as the delivery of early orders was completed, some yarn companies showed a tendency to accumulate inventory. And because the processing difference of polyester yarn continues to be high, the market price has also declined to a certain extent under the pressure of shipments. Especially in Changle, Fujian, as the main production area, the price and processing difference of polyester yarn have shown a downward trend recently.

In addition, Jiangsu’s dual-control policy has led to a certain decline in the operating rates of weaving companies and spinning mills in many places in Jiangsu. However, the operating load of local short fiber factories is generally low, and there are further production restrictions. It is expected that the inventory of local short fiber companies is generally low, and even the physical inventory is only at the 7-12 day level. Therefore, the supply shrinkage caused by the continued production reduction of short fiber companies in Jiangsu is more obvious. Next week, short fiber companies in South China are also expected to expand production cuts, so the supply of short fiber will continue to remain at a low level.

And from the perspective of polyester yarn production, although the current operating rate of polyester yarn companies has not increased significantly, it is still slightly higher than the same period in previous years. The overall market demand is still supported.

Pure polyester yarn operating rate trend chart

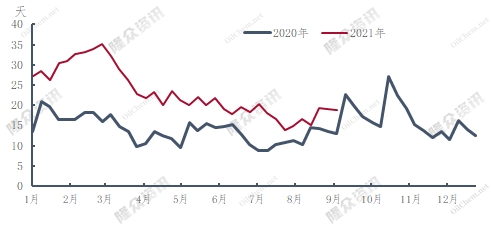

From the perspective of raw material stocking of yarn mills, the current raw material stocking of polyester yarn companies is mostly 7-20 days. Theoretically speaking, based on the current stocking days of polyester yarn companies, it is estimated that around the Mid-Autumn Festival or the National Day holiday There may have been a wave of stocking up before.

Number of raw material stocking days for pure polyester yarn companies

So although the yarn mill orders have been pending for a long time, judging from the raw material stocking and operating rate of the yarn mills, the market in September is still Keep a certain expectation of replenishment. Although the current market for polyester staple fiber is still relatively weak, with the deepening of production cuts by enterprises, the rigid demand brought about by the steady recovery of spinning mills, and the recent positive signals from Sino-US relations, polyester staple fiber is expected to rebound after oversold. It is expected; but the intensity still needs to be clearly driven. </p